The Bâloise was clearly committed to developing a stock product that is not only good for good weather conditions, but also offers security in risk markets. An established as well as transparent investment concept, which is balanced and risk-reduced on the basis of scientific processes and daily monitoring. The result is Active Risk Control (ARC), a risk overlay for fund management of a global ETF universe. The equity shares of fund-linked insurance companies are optimally controlled purely by means of quantitative algorithms and the risk of equity portfolios is therefore significantly reduced. ARC has been successful since the beginning of 2015.

The top priority of Bâloise was the security aspect. Clear processes should control the investment concept and justify our cooperation: the sole basis for investment decisions are statistical models. The development took 2 years; the result seems clear:

Risk overlay

At the beginning of the process, 10 country ETFs are selected on the basis of statistical parameters (including correlations and volatilities), which ensure the greatest possible diversification. The 10 investment possibilities are then considered separately. For this purpose, a daily test is performed on the significant change in the variance: our (already in 2011 awarded) method of structural break tests. By means of this effective risk limiter, the raincoat was constructed. Based on the structural break test, it is possible to test mathematically formally for changes in the parameters, which often change negatively in turbulent market phases. Therefore, optimal times for reinvestments within the portfolio can be determined in daily use. A stop-loss threshold then buttons up the raincoat. As an additional security feature, the algorithm triggers a sales signal when the previously defined stop-loss threshold has been torn.

Trading strategy

This is how the resulting trading strategy works: If the relevant parameters (and thus the risk) develop favorably, the proportion of promising (and hence risk-safer) investments is increased. If the risk increases on the other hand, ARC switches from risk positions to cash.

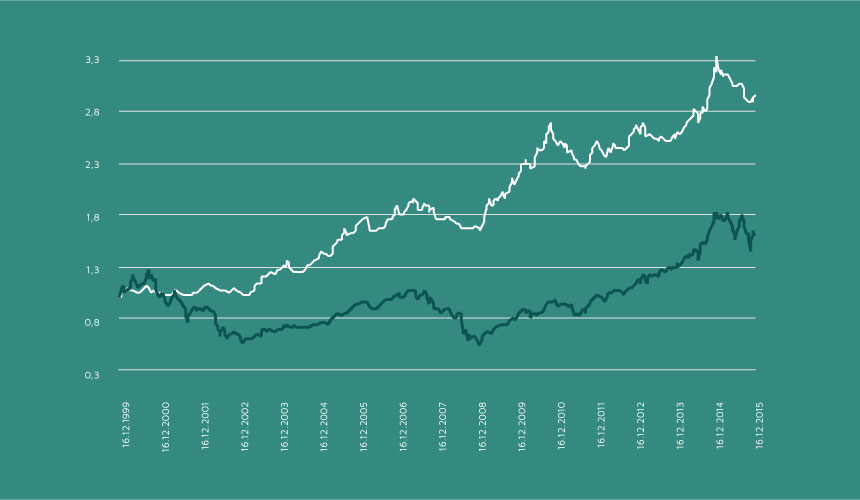

Backtest: ARC vs. MSCI in 15-years overview

Risk management

ARC uses two independent processes to control the risks. On the one hand, the widest possible diversification is striven. To this end, only country-based equity indices are taken into account and mapped via ETFs. On the other hand, the daily monitoring of the relevant market parameters as well as the loss threshold ensure a consistent protection.

The BIF – ETFSecureARC fund is managed by means of Active Risk Control and thus takes account of all claims on a clever insurance product.

Compared to the benchmark, the MSCI-World, with a 30% to 50% lower volatility.

Read more:

– Ziggel, D., Wied, D. (2011): Handelsstrategien auf Basis von Strukturbrüchen bei Korrelationen und Volatilitäten, VTAD Award 2011.

– Ziggel, D., Wied, D. (2012): Trading strategies based on new fluctuation tests, IFTA Journal, 2012, 17-20.

– Wied, D., Arnold, M., Bissantz, N., Ziggel, D. (2012): A new fluctuation test for constant variances with applications to finance, Metrika, 75(8), 1111-1127.