The terms Robo Advisor and Fintech are currently being widely talked about and are considered as the future of investment advice by numerous market observers. Regardless of whether this opinion is shared, the financial sector and, above all, the way we invest our money is facing a profound transition phase. However, it seems as if the visions and concrete implementation are running out of technical requirements and technical challenges. This is where we start.

In cooperation with FAIT Internet Software GmbH from Vienna, Quasol has developed various components to meet the increasing demand for automated investment and consulting processes. Thereby, a concrete initial situation is always assumed, and is then implemented by means of a mathematical model. For example, the following questions can be solved:

• How can a bond be optimally replaced in the portfolio?

• How can it be ensured that all customer requirements are taken into account in the portfolio?

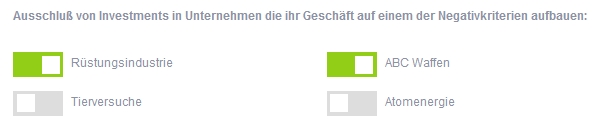

Possible customer requirements refer to e.g. the distribution of asset classes, currencies, sectors or the regional design of the portfolio. Transparency criteria can also be considered.

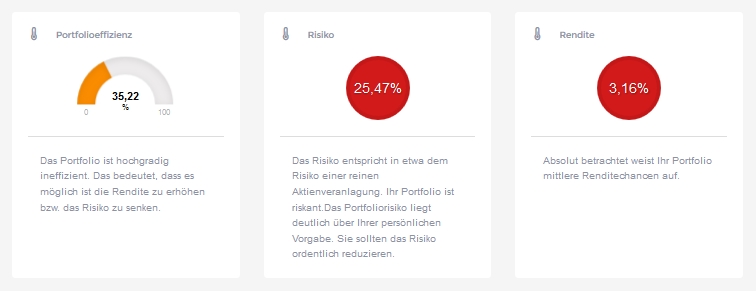

• How can the loss potential of a portfolio be reduced without having to renounce to too much return on investment?

• How can the loss potential of a portfolio be reduced without having to renounce to too much return on investment?

• How can a portfolio be optimized without having to make too many reinvestments?

All algorithms are based on the Markowitz approach and have been refined and / or extended for individual applications. The result is an extensive collection of individual and independent components, which can be used for a modern and online-based portfolio design. All components are available as web services or independent calculation core.

For first-hand experience:

We would be pleased to present the individual components online. A special show room is available for this purpose. Please do not hesitate to contact us for an appointment.

Read more:

Wied, D., Ziggel, D., Berens, T. (2013): On the application of new tests for structural changes on global minimum-variance portfolios, Statistical Papers, Vol. 54, Issue 4, pp. 955-975.